In the past year, in response to rising levels of private debt, the National Bank of Georgia (NBG) enacted new regulations to curb excessive indebtedness. There were multiple waves of initiatives. Most importantly, in May 2018 commercial banks faced certain limits in issuing the loans with real estate as a collateral, without the analysis of consumers’ solvency, while it also limited the loan to value ratio to 50%, among other constraints. On 1 January 2019, new regulation, ratified by the President of the NBG on December 24, came into force2 making full and extensive analysis of borrower’s, co-borrower’s, guarantor’s and collateral owner’s income obligatory for lenders, with restricted payments to income and loan-to-value rations. While it was also stipulated that the difference between the debtor’s net income and monthly repayment on total obligations must be higher than the subsistence minimum for the working age. The impacts of the implemented regulations are as yet unclear but generally the reaction in the private sector has been negative3. In this

newsletter, a brief overview of the possible implications of these lending regulations are presented.

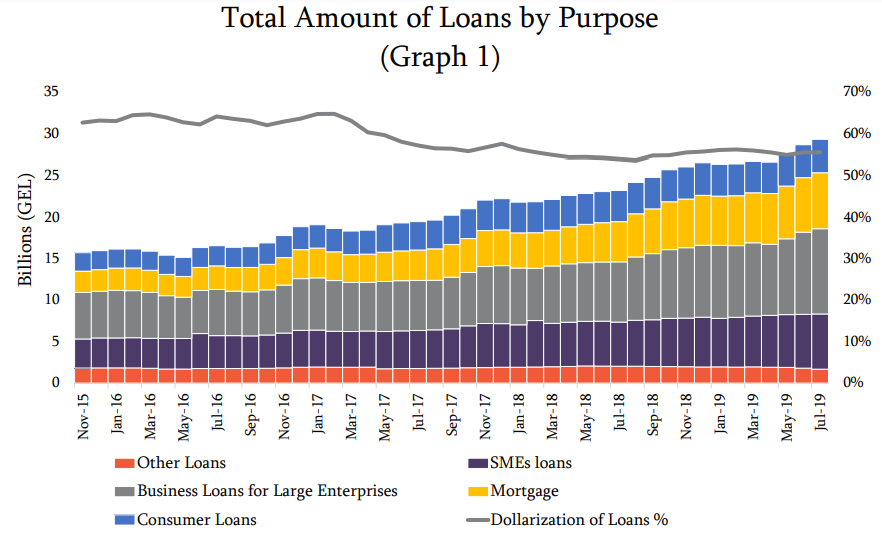

In July 2019, total loans issued to the national economy made up GEL 29.34 billion4 (including overdue loans) amounted to 71% of the GDP, which was 26.1% higher compared to the same indicator for the same month the previous year. In particular, three types of loans contribute more than 80% of the total debt: business loans for large enterprises (35.01%); loans for small and medium-sized enterprises (SMEs) (22.72%);

and mortgages (23.01%) (See graph 1). As the dollarization rate, or the amount that is lent in foreign currency, is at 56%, Lari depreciation is inflating more than half of the debt, making growth comparison between different loans overtime defective. (And excluding this effect would decrease the total loans growth to 14.8%).

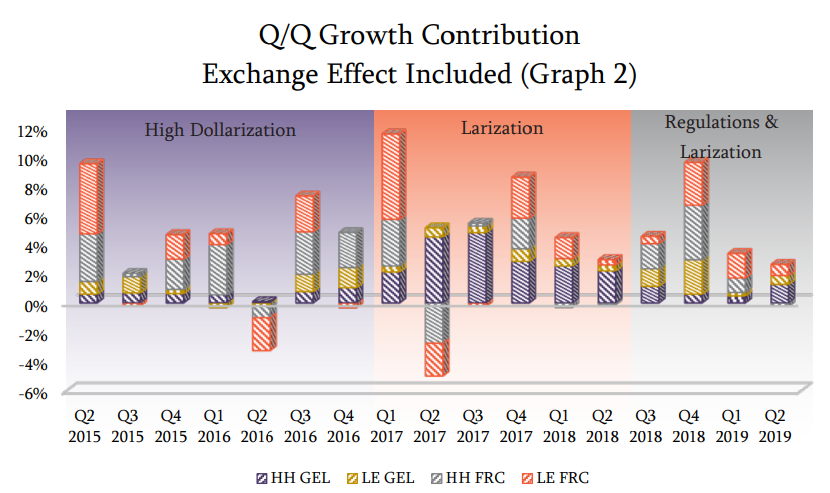

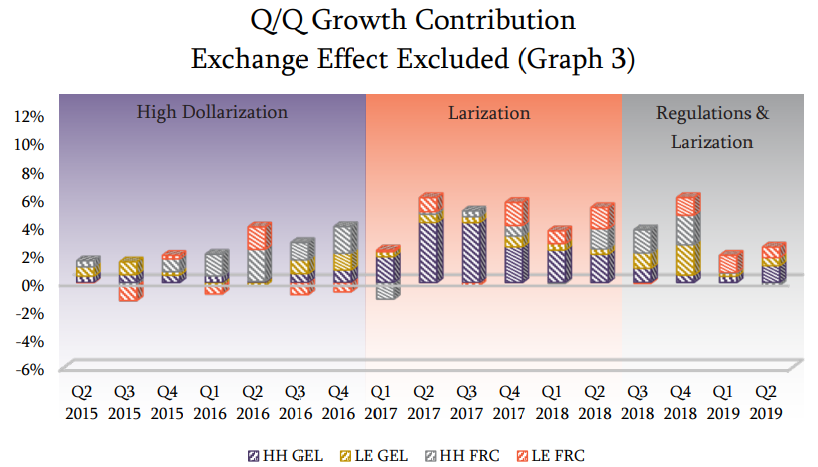

For simplicity, the total loans can be divided into four parts: loans issued to households (HH); loans issued to legal entities (LE); loans issued in GEL; and loans issued in any other foreign currency (FRC). As can be seen from graph 2, in 2015-2016 the main contributors to total debt growth have been household and legal entity loans in foreign currencies. Meanwhile, when the effect of the currency exchange rate is taken into account (see graph 35), a significant part of quarter-over-quarter (Q/Q) growth contribution shifted to household loans issued in domestic currency, mainly due to the measures implemented under the so-called Larization policy in January 20176. However, in the third quarter of 2018, when the first wave of regulations was implemented, growth of household loans issued in national currency considerably slowed down. The household loans issued in foreign currencies followed the same path after the January 2019 regulations. Both trends are discussed separately below.

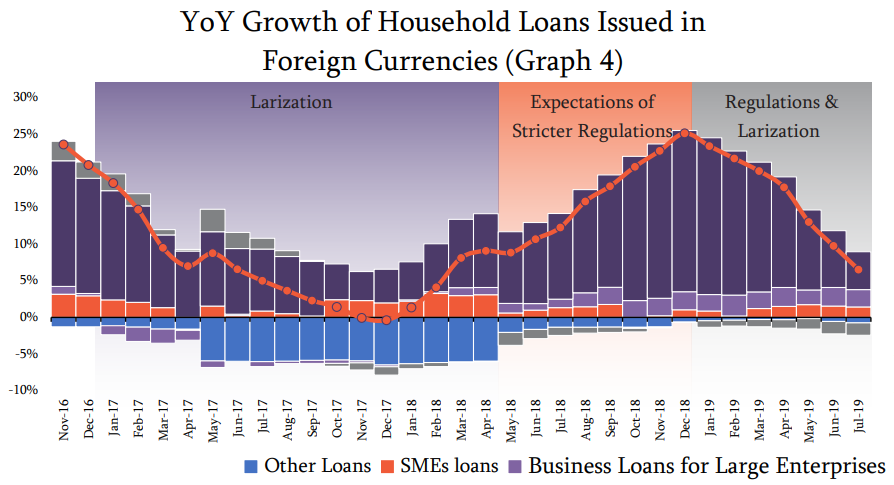

In December 2017, 11 months after the tightening of lending for households in foreign currency (Larization), the year-over-year (YoY) growth of household loans issued in foreign currencies reached its lowest point in four years as the aforementioned loans decreased by 0.38%. Thereafter, a sudden surge in household mortgages issued in foreign currencies ensued, which may be attributed to expectations of stricter mortgage

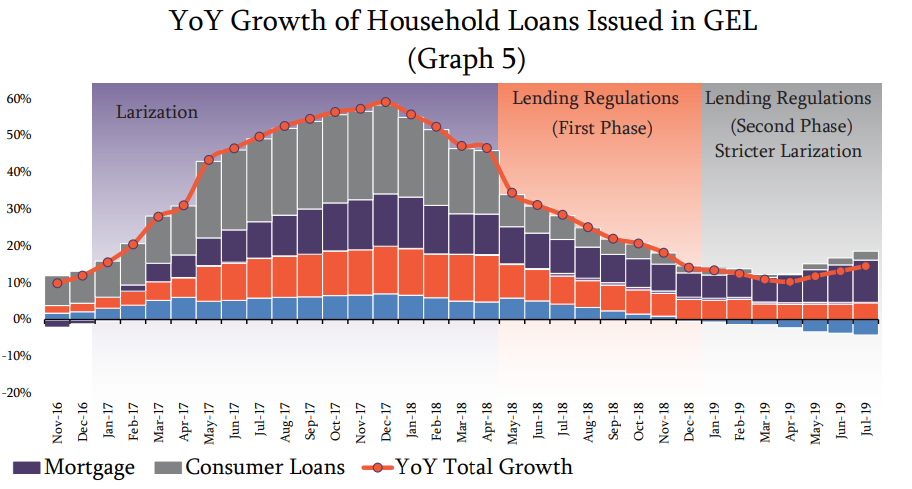

regulations and more stringent Larization policy (see graph 4). That growth was cut abruptly by the January 2019 lending regulations and stricter Larization policy7. Meanwhile, the fall in growth of household loans growth issued in GEL was mainly due to a slowdown in consumer loans, the sharp decrease of which can be seen after May 2018 regulations, when its contribution to the total year-over-year growth dropped from 17.24% to 8.75% (see graph 5). This has been decreasing ever since. It is interesting to note that after the further expansion of the“Larization” policy in January 2019, growth of household loans issued in GEL has stabilized, primarliy due to marginal increases in mortgage loans in GEL.

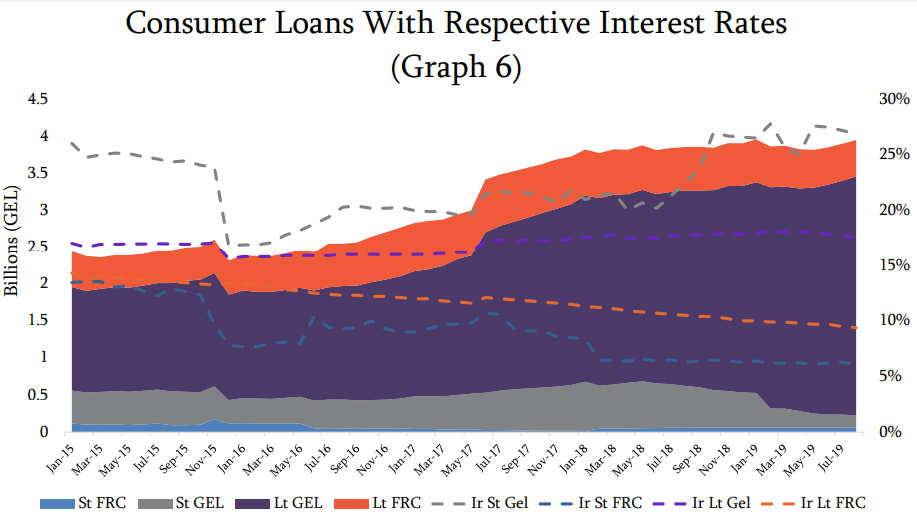

The stagnation in consumer loan growth can be more comprehensively understood by breaking it down according to primary maturities (shortterm and long-term) and the currency it is issued in (GEL or FRC), with

their respective interest rates (Ir) (see graph 6). A sharp decrease in short-term consumer loans issued in GEL (St GEL) can be observed in January 20198. The new regulations could have played a significant role in reducing short-term consumer loans issued in domestic currency.

Interestingly, in only 6 months average interest rates for short-term consumer loans in domestic currency (Ir St GEL) had increased by 5 percentage points, while for every other type of consumer loan the interest rates decreased. It can also be observed that the percentage of consumer loans issued in short-term maturity decreased from 17.9% to 5.8% after the regulations of May 2018.

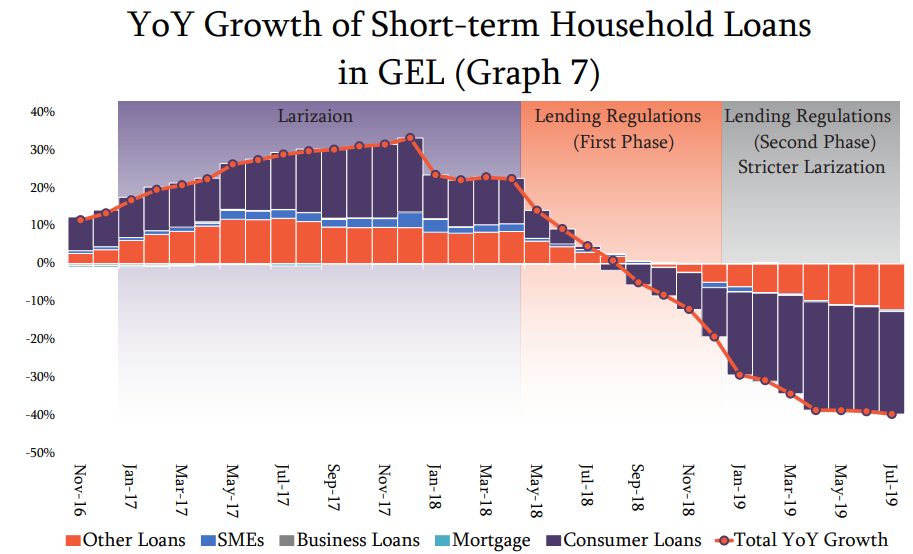

With it year-over-year growth of short-term loans for households has also been decreasing, mainly because of the reduction in consumer loans and “other loans” (see graph 7). Meanwhile, since the introduction of the Larization policy in January 2017, long-term consumer loans in GEL have increased by 61.9%, while its share dropped from 42.8% to 81.8%.

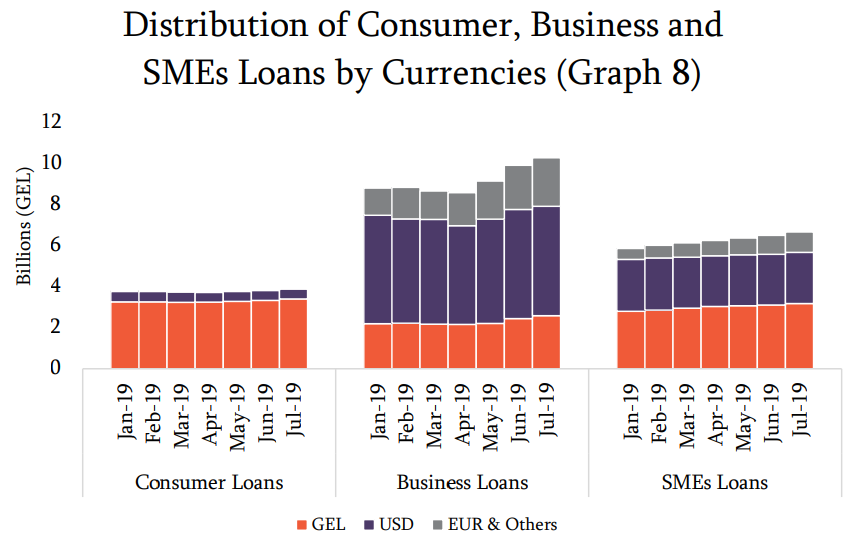

According to a statement made by the President of the NBG9, one of the consequences of these regulations was that the funds have been redirected from consumer and large corporation (business) loans to SME loans. From January until August of this year, consumer loans have increased by 3.37%, business loans have increased by 16.75%, and SME loans have increased by 13.78%. It is important to note that most (74.83%) business loans are issued in USD and EUR, while the percentage of SME loans issued in foreign currencies is 52.4%, and for consumer loans it is 17% (see graph 8). However, when the currency exchange rate fluctuations are taken into the account, growth of business loans in the current year decreases to 10.77%, consumer loans drops to 1.94% and SME loans decreases to 9.59%, reflecting more favorable growth for SMEs, compared to 6.59% in the same period of the previous year. Much like consumer loans, growth in mortgage loans has also declined: in the first seven months of the current year it increased by 13.43%, but after taking into account the exchange rate effect this drops to 7.58%, which is almost two-and-ahalf times less than in the first seven months of 2018 (18.12%).

Such a significant slowdown in consumer loans and mortgages this year could be reflected in the net profits of commercial banks and microfinance organizations. In particular, the net profits of all 15 commercial banks combined in the first two quarters equaled 559.376 million GEL, which is 12.96% less compared to the same period of the previous year. Meanwhile, microfinance organizations have recorded a net loss of GEL 66.221 million this year, which is particularly concerning as they recorded net profits of GEL 89.221 million for the whole of 2018. For comparison, in the fourth quarter of 2016 alone, total net profits made up a staggering 151.853 million GEL. Furthermore, since the second quarter of the last year, the value of online loans issued to individuals by the aforementioned organizations dropped by 64.53% year-over-year, while loans issued to legal entities has increased by 51.27%. In the same 2018-2019 period, the total number of microfinance organizations and the number of employees in those sectors has decreased. In the second quarter of 2018, there were 70 such organizations operating, but the number has decreased to 56 (a reduction of 20%).

Source - PMCG