As of the 2nd of July, the GEL REER is strongly undervalued and is likely to strengthen going forward (see more in TBC Research quick update: “The CA deficit improved and the GEL undervalued” and forthcoming monthly update).

No GEL call options* are sold by the central bank, implying no automatic interventions if the GEL appreciates below its 20 day moving average.

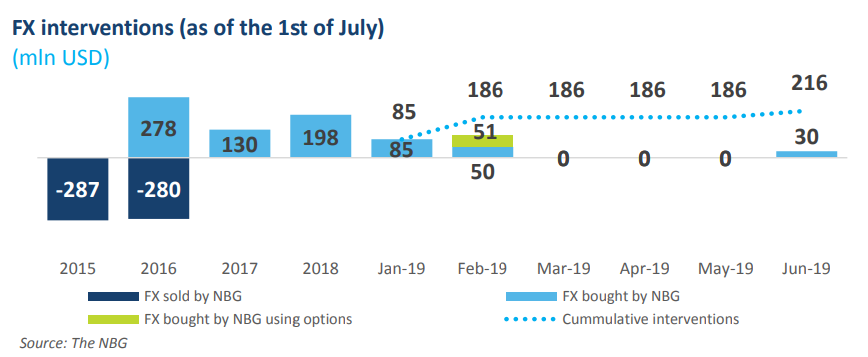

Considering the NBG has already bought a substantial amount of reserves and the GEL has significantly weakened posing inflationary risks, it is highly unlikely that the NBG will buy reserves if the GEL strengthens in coming weeks.

Source - TBC Research