-

“The purpose is to rein in Ma Yun,” said an adviser to China’s State Council, the country’s top government body, using Mr. Ma’s Chinese name. “It’s like putting a bridle on a horse.”

- “I think among the richest men in China, few have good endings.” - Jack M

Beijing’s protracted dismemberment of Jack Ma Inc. continues.

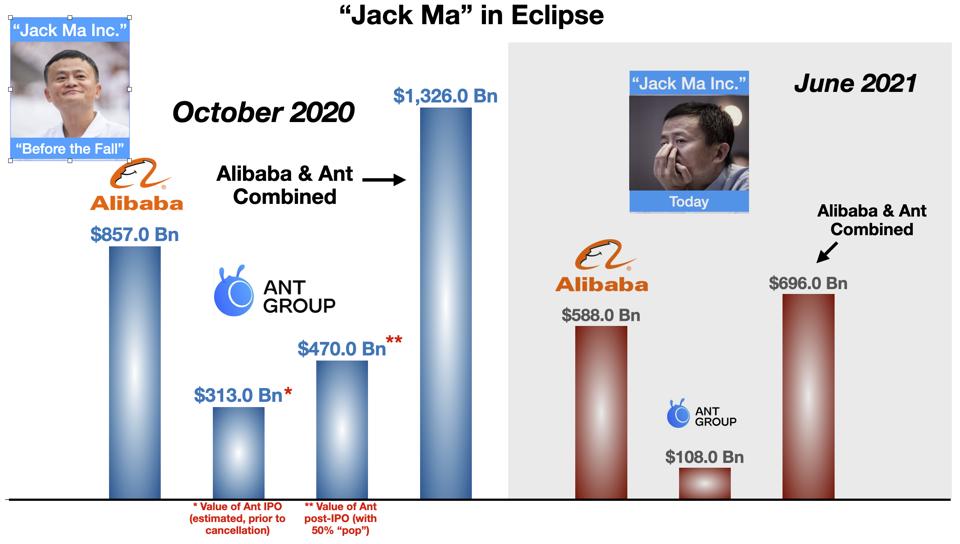

“Bridle on the horse” hardly describes this orgy of value destruction. This “horse” has suffered multiple amputations, performed without finesse by the Chinese government. The Ma empire is worth half what it was 9 months ago.

The process is not over. Beijing is now doling out some of the most lucrative slices of Ma’s business to new “partners” of its choosing, including one of the most corrupt and financially shaky companies in all of China.

Who Was Jack Ma?

One year ago, Ma was the richest man in China. He was the creator of Alibaba – China’s largest tech company – and The Ant Group, the largest Fintech company in the world. His corporate empire had reached private-sector superpower status, on a par with the Western FANG-giants. Alibaba alone was worth more than any U.S. company except for Apple, Amazon and Google.

Ma was also a worldwide celebrity – the most famous living Chinese person. According to polls he was more well-known outside China than Xi Jinping. Jack Ma was Jeff Bezos, Elon Musk and Bill Gates all rolled into one. He was the front-man for the new China:

- “It is hard to overstate the importance in China of Mr. Ma and his two companies. They have become synonymous to innovation. The media in China calls the country’s rising tech sector, ‘The era of Ma.’”

The abrupt reversal of his fortunes has been shocking to watch. Ma’s assets have been stripped, shorn, and degraded (“rectified” is the English word often given as the translation for whatever verb in Chinese describes what Beijing is doing to his businesses).

The Rectifications

The Canceled Ant IPO

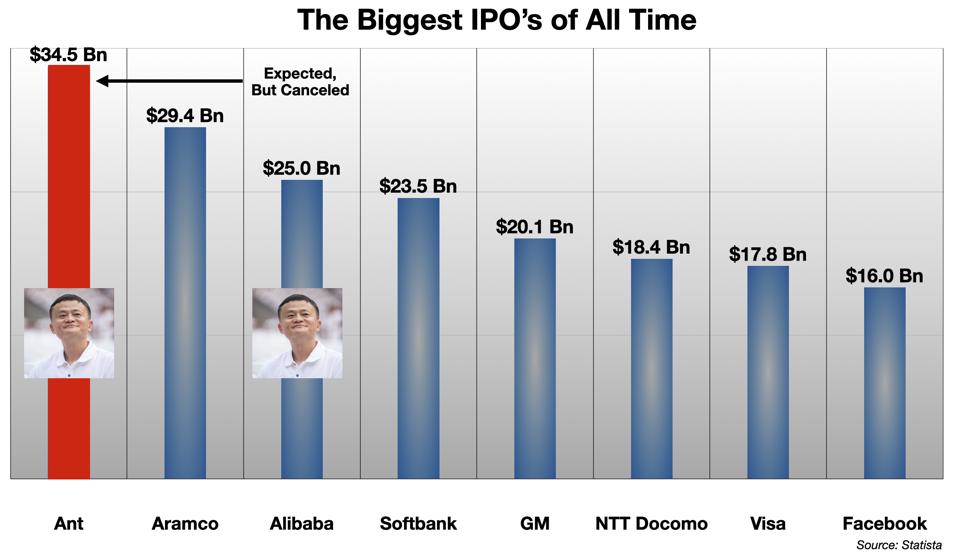

The last-minute quashing of the Ant Group’s Initial Public Offering was the opening shot (which I wrote about at some length last year). The offering would have set a world record. (In fact, Alibaba’s IPO in 2014 had been the largest ever at that time. Ant’s was to have surpassed it by 40%.)

The size of the deal itself doesn’t portray the scale of the financial phenomenon. The Ant IPO had become – by October 2020 – a true frenzy. The share price on the private market ran up 50% ahead of the effective date, and the offering was said to have been 80 times oversubscribed. The Wall Street Journal called it “a $3 trillion scramble.”

Ma was triumphant. It would be, he said,

- “the biggest IPO in human history. Furthermore, for the first time ever, it is set in a city other than New York . . . A miracle is happening.”

The WSJ reported that the order book exceeded “the value of all the stocks listed on the exchanges of Germany.”

Then — Beijing killed the deal.

Carving up the Company

Following the IPO fiasco, regulators began to disassemble Ant. Its consumer financing business was set to be restructured, with new “partners.”

- “The central bank ordered Ant to form a separate financial holding company that would be subject to the kind of capital requirements applied to banks. That could open a door for big state banks or other types of government-controlled entities to buy into the firm.”

The government also had its eye on one of Ant’s most valuable assets - its data, derived from billions of consumer transactions it processes. The tech-intensive analytics generated from this resource have been the basis of Ant’s competitive advantage over the less technologically sophisticated traditional banking sector in making consumer credit decisions. Beijing aimed to “rectify” that, too.

- “Ant will also be required to break an “information monopoly” on the vast and detailed consumer data it has collected, the central bank said.”

- “Hiving off the treasure trove of data on more than 1 billion people is a key part of Ant’s business overhaul in response to a regulatory crackdown.”

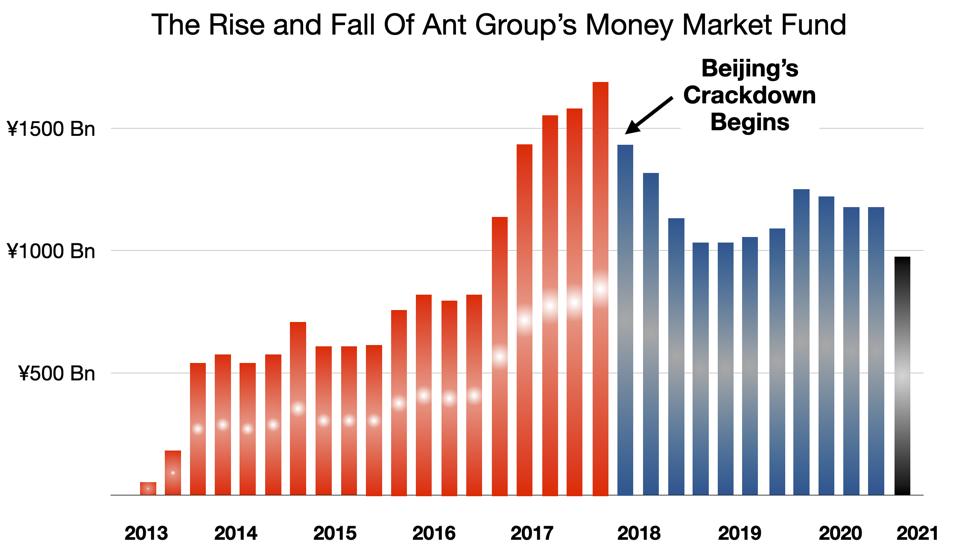

Neutering Ant’s Money Market Fund

Ant’s Group’s money market fund was perhaps its most amazing and explosive success story. In just four years, the fund became (briefly) the world’s largest, surpassing the American establishment giants like Fidelity and JP Morgan and “shocking banking executives around the world.” Ant built this fund up by inviting Chinese consumers to hold their spare cash (“leftover treasure” in Chinese) in these accounts.

Beijing took note. Ant’s business was thrown into reverse, shrinking 18% in the first quarter of this year, and down almost 50% from its peak.

This decline is not (as has been suggested by some) due to “natural” market forces, interest rate shifts, or trends in the Chinese equity markets. It is the direct result of Beijing in action.

- “Ant Group’s money market fund has shrunk to a more than four-year low as users shifted their cash in the face of China’s crackdown on Jack Ma’s payments group… Ant was ordered to “actively reduce” [the fund’s] size as part of a restructuring deal struck with Chinese authorities last week.”

Antitrust Penalties

In April, a “record” fine of $2.8 Bn was levied against Jack Ma’s flagship, Alibaba – for antitrust violations. The dollar amount appeared far smaller than the financial damage from the broken Ant IPO, and some observers dismissed it. Still, it was the description of the “sin” that mattered. The company was accused of “abusing its market dominance” and, again, “ordered the company to ‘rectify’ its behavior” and “shrink its business.”

- “The regulator’s punishment of Alibaba Group is a move to standardize the company’s development and set it on the right path, to purify the industry and to forcefully protect fair competition in the market.”

(“Standardize,” “Purify,” “Set on the Right Path”… The pronouncement rings with Orwellian cadences. And who would ever have thought to hear about “protecting fair competition” from the communists?)

“Minor” Harassment

Chinese authorities have piled on other penalties, which seem minor, or tangential, but in context they display Beijing’s animus even in petty matters.

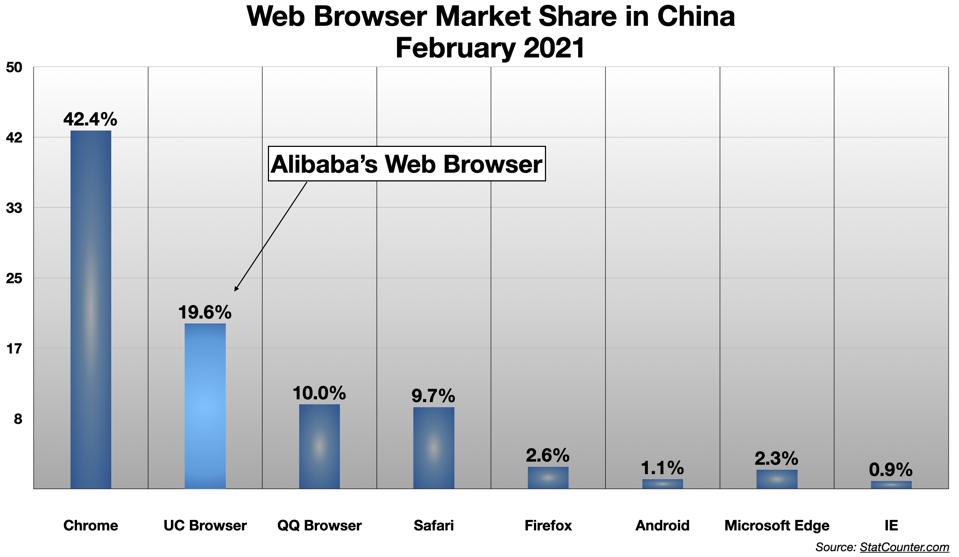

For example, the company’s highly popular Internet browser – number 2 in the Chinese market with over 400 million active users – was deleted at Beijing’s insistence from the app stores of most mobile and Internet companies in March.

In April, Beijing announced an investigation into the Ant’s dealings with the Shanghai stock exchange to obtain approval for the IPO. Insider dealing and quasi-corruption were implied:

- “The probe examines how an array of state funds, including massive sovereign-wealth fund China Investment Corp. and the country’s largest state insurers—among them China Life Insurance Co. — got to invest in Ant… Listing standards and procedures set by both the China Securities Regulatory Commission and stock regulators in Shanghai are under scrutiny. The way Ant’s IPO application was handled fueled Mr. Xi’s concerns the state’s interests weren’t being adequately protected.”

Closing Ma’s Hupan University

Also in April, Ma was removed as president of Hupan University, the ultra-elite business school he founded and endowed in 2015.

This is to my mind the saddest of all these injuries. The plan for Hupan was ambitious, bold, innovative. It promised a fresh approach to business education, in some respects going beyond anything done elsewhere.

- “After a rigorous, six-month selection process, Jack Ma’s Hupan University announced the commencement of its new student class. More than 40 CEOs from Chinese tech unicorns were welcomed to the program, which promises to be one of the most powerful business networks in the country.However, the program is more famous for its powerful alumni that clearly influence China’s technology business sector. While only 207 Chinese corporate executives are among the school’s alumni, they include many well-known names.… A qualified applicant must head a startup which earns a minimum of RMB 30 million (around $4.5 million) in revenue, has paid taxes for more than three years, and has at least 30 employees.”

As an educator myself, I was impressed with this model. It fit with China’s desire to leapfrog the slower, more organic American approach to business education, and combined what we would call “advanced Exec Ed” with an intensive shared personal experience and network cultivation. The closest thing to this in the U.S. is the Harvard Business School, and Ma wanted to go even further. It was a grand vision.

It was working:

- “Hupan quickly became one of China’s most prestigious business schools.”

- “We want Hupan to run for 300 years.” - Jack Ma

Beijing will now apparently dismantle the whole thing. “The Chinese Communist party has grown increasingly suspicious…

- “Jack Ma’s elite business academy has been forced to suspend new student enrollments following pressure from Beijing as authorities tighten their chokehold on the Chinese tech billionaire’s empire.”

- “Ma needs to disassociate himself from the organisation but there are worries that Hupan may have trouble attracting students if Ma exits completely,” one person said. “The academy is popular because of him, not its curriculum.”

Huarong

Now, the worst of it –

It was reported last week that “regulators approved Jack Ma’s Ant Group to start running a new finance company.” It will absorb the most profitable part of Ant — the consumer lending business. Ant will contribute its massive portfolio of $155 Bn in outstanding loans.

- “The unit will become the centerpiece of Ant’s restructured lending business, which had grown so large that it issued about one-tenth of China’s non-mortgage consumer loans last year.”

However, Ant will now own just 50% of the new company - to be called Chongqing Ant Consumer Finance. Ant even has to pay another $625 million for a half-stake in its own business! The other 50% is being handed out to several new “partners” (who apparently are not required to make capital commitments). They include a battery company (?), a manufacturer of video surveillance equipment, and, yes, an actual bank, though it is a wholly owned subsidiary of one of the state-owned “bad banks” set up in the 1990s to process massive amounts of non-performing loans that were choking the state banking sector at that time.

But the real shock is who gets the final seat at the boardroom table: Huarong Asset Management. They are being given 4.99% of the business, for nothing it seems.

Huarong is the most notorious bad actor in all of Chinese finance.

- The company was created as another one of the “bad banks” in the 90s – and so was swimming in polluted waters from the start, trafficking in bad loans

- It later expanded its business recklessly into many other areas outside its charter, including large, risky foreign private investments; it is even today not entirely clear to Chinese authorities what it owns

- Huarong developed a culture of massive and systematic corruption, led by its CEO Lai Xiaomin, until his downfall in 2018 — the company became a media “villain” in China, an example of fraud and incompetence, the subject of a lurid TV series and documentaries that aired on national networks

- This year, Huarong has flirted with bankruptcy, as its past sins catch up with it – it is the largest Chinese issuer of dollar-denominated foreign debt – $22 Bn – and is said to be on the edge of default, which may provoke a regulatory crisis (because of its majority state ownership)

- Huarong’s troubles threaten the integrity of the larger fixed income market in China, and could force a government bailout

Oh, and in January 2021, former CEO Lai Xiaomin was executed for bribery, “greed” and other sins.

Bringing Huarong into this venture shows that someone in Beijing has a nasty sense of humor. It’s as though the U.S. government had said to Facebook, “Mr. Zuckerberg, say Hello to your new partner, Bernie Madoff.”

Media reports portrayed this new deal as a “thaw” and an “easing of tensions” — a “green light” for Jack Ma. But the addition of Huarong feels like mockery, or even contempt, on the part of Beijing’s regulators for Mr. Ma and what he represents. To tie the most dynamic and innovative high-tech entrepreneur China has produced so far to a corrupt, bankrupt, sluggish, thuggish and incompetent wreck of a company… What can that signify, except contempt?

It is at the very least a message, and a warning, to the rest of the private sector. It is also another strategic blunder on China’s part – but that is for a future column.