By Levan Kokaia:

Strategic Advisor in Renewable Energy.

Lawyer at Georgian Renewable Energy Development Association (GREDA).

Introduction

Georgia’s ambition to position itself as a regional hub for clean and sustainable energy requires not only strong policy direction but also a financing ecosystem capable of mobilizing large-scale capital. As global investment trends shift sharply toward green finance, countries with well-developed capital-market instruments, transparent regulatory frameworks and robust environmental standards increasingly attract international investors seeking long-term, impact-oriented opportunities. For Georgia strategically located between Europe and Asia and endowed with abundant hydropower, strong solar potential and emerging wind resources - the window to align with global green capital flows is both timely and crucial.

Historically, Georgia’s renewable energy projects have relied heavily on a combination of commercial bank lending and IFI-supported financing. While these channels have enabled the construction of numerous hydropower plants and the country’s first utility-scale wind projects, they alone are insufficient to deliver the next decade of energy transformation. Grid upgrades, solar and wind acceleration, energy storage systems and regional market integration will require financing volumes that exceed the capacity of banks and IFIs combined.

To unlock broader investor participation, Georgia must begin shifting toward capital market-based green financing instruments, with green bonds at the center of this transition. Experiences from EU member states demonstrate that well-structured green bond frameworks aligned with EU taxonomies and backed by credible reporting can catalyze billions in private capital for renewable energy, transmission infrastructure and climate-aligned corporate expansion. Georgia holds similar potential, provided that the right enabling environment is established.

The following sections explore how Georgia’s current financing landscape is evolving and how the country can apply lessons from successful international green bond markets.

1. The Evolving Role of Commercial Banks in Georgia

Georgia’s commercial banking sector has traditionally served as the backbone of project financing in the renewable energy space. Major institutions have developed specialized lending strategies for hydropower, solar and wind projects. Supported by credit lines and risk-sharing facilities from IFIs, these banks have accumulated technical expertise and improved their understanding of sectoral risks.

However, several structural constraints limit the ability of banks to scale financing for a national clean energy transition:

·Tenor Limitations

Typical bank loans in Georgia range from 5 to 10 years, which is often misaligned with renewable energy project lifecycles of 20–30 years. Shorter maturities require higher annual debt service payments, reducing feasibility for developers.

- High Collateral Requirements

Banks commonly require collateral valued at 120–150% of the loan amount, often secured through real estate or the project assets themselves. This poses challenges for developers with land-use rights or concessions but limited tangible assets.

- Risk Aversion in Early-Stage Projects

Feasibility-phase financing, such as permitting, environmental studies or grid connection assessments is rarely supported. Developers shoulder early-stage risks alone, limiting pipeline development.

- Concentration Limits

Given the banking sector’s size, exposure thresholds prevent institutions from lending large amounts to a single corporate group or sector. This becomes a particular challenge for large utility-scale wind or solar farms.

As renewable technology costs decline globally and Georgia seeks to diversify beyond hydropower, the demand for financing will increase. To ensure bank lending remains effective, it must be complemented by capital market solutions, blended finance and long-term institutional investment.

2. The Role of International Financial Institutions (IFIs)

International financial institutions such as the World Bank, EBRD, IFC, ADB have historically played a central role in shaping Georgia’s renewable energy sector. Their contributions extend far beyond traditional lending and include:

·Long-Term Project Finance

IFIs are often the only institutions willing to provide 12–18-year maturities, matching the cash-flow profiles of renewable energy assets.

- Technical Assistance & Capacity Building

IFI support has been crucial in environmental impact assessments, climate resilience planning and grid integration studies.

- De-Risking Instruments

Guarantees, political risk insurance and liquidity buffers provided by IFIs make previously unbackable projects financeable.

- Catalyzing Commercial Co-Financing

Banks are more willing to lend when an IFI serves as an anchor investor or co-financier. Despite their importance, IFIs alone cannot meet the capital requirements for Georgia’s full-scale transition to a diversified renewable energy system. IFI funding tends to be selective and cannot replace market-driven financing. Thus, their strategic role should shift from direct financing to mobilization, where IFIs help develop local capital markets, guide taxonomy adoption and support the inaugural issuance of green financial instruments, similar to their role in many EU countries.

3. Green Bonds as a Strategic Opportunity

Although the global green bond market surpassed $2 trillion in cumulative issuances, Georgia has yet to issue its first domestic green bond dedicated to renewable energy. This represents a missed opportunity but also a powerful untapped potential.

Why Green Bonds Matter for Georgia?

·Lower Cost of Capital

ESG-oriented investors often accept lower yields, reducing financing costs for project sponsors.

- Longer Maturities

Green bonds typically carry tenors of 7-15 years, enabling project-aligned repayment schedules.

- Access to Institutional Investors

Pension funds, impact investors, sovereign wealth funds and large asset managers prefer labelled instruments with transparent sustainability commitments.

·Enhanced Market Credibility

A national green bond, whether sovereign or corporate would signal Georgia’s commitment to sustainability, improving investor confidence across sectors.

·Alignment with EU Integration

Georgia’s movement toward adopting EU Green Taxonomy principles will further support investor trust and compliance with international reporting expectations. The optimal path forward for Georgia could include: a sovereign green bond to establish market benchmarks, corporate green bonds issued by major energy developers, green project bonds for single assets and financial institution green bonds to support lending portfolios. The EU experience shows that once the first benchmark issuance occurs, market participation typically accelerates rapidly.

4. EU Case Studies

To better understand how Georgia can design its own pathway, several EU member states offer relevant and practical examples.

Case Study 1: Poland. PGE’s Green Bond for Offshore Wind & Grid Modernization

Poland’s energy transition relies heavily on expanding offshore wind and modernizing transmission networks. State-owned utility PGE issued a €500 million green bond aligned with the EU Taxonomy and ICMA Green Bond Principles (GBP).

Key Success Factors were: strong state commitment to renewable energy targets, clear and transparent corporate green financing framework, annual impact reporting, including emissions reductions and grid improvements and high investor participation due to policy clarity.

Why it Matters for Georgia: GSE or another state-owned energy entity could adopt similar frameworks to finance urgently needed transmission upgrades, supporting future solar and wind integration.

Case Study 2: Lithuania. Ignitis Group’s Multi-Billion Euro Green Bond Program

Lithuania has become a Baltic leader in renewable energy finance through the success of Ignitis Group, which issued more than €1.1 billion in green bonds across several tranches.

Success drivers were: rapid adoption of EU Taxonomy-aligned rules, clear decarbonization strategies by utilities, strong regional investor appetite and government support for corporate bond issuance.

Relevance for Georgia: Georgian developers - especially those with operations in neighboring countries could similarly leverage international exchanges to expand their financing capacity.

Case Study 3: Spain. Sovereign and Corporate Green Bonds Powering Solar Expansion

Spain is among Europe’s most active green bond markets. The Spanish government launched sovereign green bonds that quickly became reference points for the market. Companies such as Acciona and Iberdrola have raised billions for solar PV and grid infrastructure through labelled debt.

Core lessons are the following: sovereign green bonds create market confidence; clear permitting reforms accelerate project readiness and harmonization with EU sustainability standards attracts global investors.

Relevance for Georgia: A sovereign green bond could set a benchmark yield curve for Georgian corporates and open the market for multiple sectors, not just energy.

5. Alternative Financing Models

While green bonds represent perhaps the most visible mechanism for scaling investment in Georgia’s renewable energy sector, they are only one component of a broader financing architecture. A mature clean-energy market requires an ecosystem of diversified instruments capable of addressing varying risk profiles, project stages and investor preferences.

·Sustainability-Linked Loans (SLLs)

Unlike green bonds, which earmark proceeds for specific green projects, SLLs tie the cost of capital to the borrower’s sustainability performance. Metrics may include emission reductions, renewable generation volumes or improvements in corporate governance. For Georgia, SLLs offer several advantages. In particular: they can be issued by existing corporate entities without creating project-specific vehicles; banks in Georgia, especially those with strong IFI partnerships can integrate SLL products with minimal regulatory changes; they incentivize companies to adopt broader ESG improvements across all operations.

·Infrastructure Investment Trusts (InvITs)

InvITs are popular in South-East Asia allow income-generating infrastructure assets to be pooled and listed on stock exchanges. Investors receive stable, long-term dividends. For Georgia, InvITs could provide an exit mechanism for early-stage developers and attract regional pension funds and impact investors. Also, it increases liquidity in domestic capital markets. Though regulatory adjustments are required, InvITs could become a cornerstone instrument for scaling mature hydropower and wind assets.

- Crowdfunding and Community-Based Renewable Financing

As demonstrated in Germany, Belgium, and the UK, community ownership models can significantly enhance social acceptance of renewable projects while diversifying financing sources.

In Georgia, crowdfunding could support rooftop solar adoption, small municipal renewable projects and rural electrification and storage initiatives. Such models align well with Georgia’s decentralized energy development goals and can foster citizen participation in the energy transition.

Diversified financing mechanisms not only expand the capital available for renewable projects but also build resilience into Georgia’s financial landscape, reducing over-reliance on banks and IFIs.

6. ESG & Corporate Governance

As global investors increasingly priorities sustainability, compliance with environmental, social and governance (ESG) standards has become indispensable for accessing long-term institutional capital. For Georgia’s renewable energy sector, strengthening ESG and corporate governance frameworks is essential not only for financing but also for enhancing project credibility and reducing perceived risks.

·ESG as a Precondition for Capital Market Access

In the EU and US markets, investors routinely screen potential issuers based on: climate risk exposures, biodiversity protection measures, stakeholder engagement processes, supply chain transparency issuers that cannot demonstrate robust ESG performance face higher borrowing costs or exclusion from investment portfolios. For Georgia, adopting internationally recognized frameworks such as ICMA, TCFD, SASB and EU Taxonomy will be crucial.

·Corporate Governance as a Risk Mitigation Tool

Strong corporate governance practices directly influence investor confidence. This includes: transparent decision-making structures, independent supervisory boards, clear anti-corruption mechanisms and public disclosure of financial and non-financial performance.

·Social and Community Engagement

For large hydropower or wind projects, social acceptance often determines project success.

Adopting clear stakeholder engagement strategies, benefit-sharing mechanisms and grievance redress procedures significantly reduces project delays and enhances investor trust.

·ESG as a National Branding Strategy

Countries that pioneer sustainability reporting and green taxonomies like Lithuania and Slovenia attract disproportionately high levels of capital relative to their market size. Georgia has an opportunity to position itself as a regional leader in green governance by integrating ESG standards into national energy, investment and corporate reporting frameworks.

7. Conclusion

Georgia stands at a strategic crossroads in its clean-energy development. With abundant natural resources, strong regional interconnections and growing investor interest in sustainable markets, the country has all the preconditions to become a leading renewable energy hub in the South Caucasus. Yet achieving this vision requires a financing ecosystem capable of mobilizing capital at scale.

The evolution of commercial banking, combined with the catalytic role of IFIs, it has built a solid foundation. However, the future of Georgia’s clean-energy transition lies increasingly in capital market solutions. Green bonds when aligned with EU Taxonomy principles, supported by transparent reporting and backed by strong ESG and governance practices can unlock entirely new pools of investors, extend project tenors and reduce financing costs.

International experience demonstrates that even small economies can access global green capital if the right frameworks are in place. By adopting best practices from the EU, leveraging alternative financing tools and building investor confidence through ESG excellence, Georgia can accelerate renewable deployment, modernize its energy infrastructure and strengthen its economic resilience. The moment is timely, the capital is available and the opportunity is substantial. Georgia’s next step is to embrace market-driven green financing as a central pillar of its sustainable energy future.

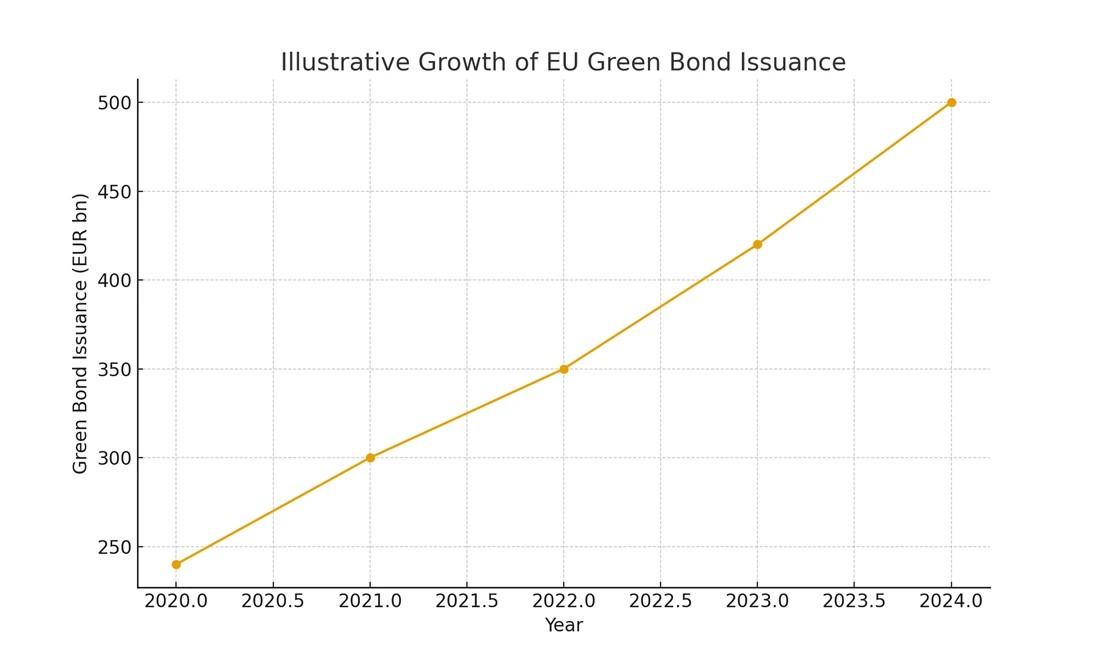

For illustrative purposes, the following chart highlights the growth of Green Bond issuance across the EU:

Illustrative Table: Sample Green Bond Framework Elements:

|

Framework Component |

Description |

|

Use of Proceeds |

Renewable energy, energy storage and grid modernization. |

|

Reporting |

Annual impact reports aligned with ICMA standards. |

|

Verification |

External review by accredited verification bodies. |